The volatile swings of some Indonesian shares have earned them the nickname saham gorengan or ‘deep fried stocks’, with their restricted floats and concentrated ownership contributing to rallies that can lift their tycoon owners into the ranks of Asia’s richest people almost overnight.

In recent days, index provider MSCI has shone a light on this practice, threatening to downgrade Indonesia to a frontier market unless it cleans up its act by May.

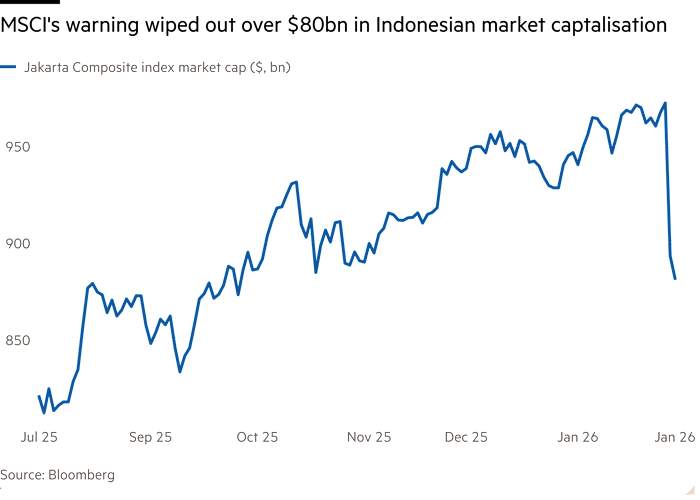

The announcement — citing “opacity in shareholding structures and concerns about possible co-ordinated trading behaviour that undermines proper price formation” — wiped nearly $80bn off the Jakarta Composite index last week and sent financial regulators scrambling to prevent a reclassification that could trigger billions of dollars in capital outflows.

Stocks fell a further 4.5 per cent on Monday.

Already, authorities have taken action, announcing plans to double the free-float minimum to 15 per cent in an attempt to boost liquidity and lower volatility. Shares in companies with low free floats can fluctuate wildly due to thin trading.

The heads of Indonesia’s financial regulator and stock exchange have resigned.

“This is surely just a temporary shock because there is no issue in our fundamentals,” finance minister Purbaya Yudhi Sadewa said of the market sell-off after the MSCI announcement. Purbaya is among those to have repeatedly called for a clean-up of the Indonesian market.

The MSCI announcement comes amid broader concerns about President Prabowo Subianto’s loose fiscal policy and threats to central bank independence.

In recent months, Prabowo nominated his nephew to the central bank, which investors and analysts see as an attempt to make the bank more pro-growth at the expense of a weaker rupiah and rising inflation. Prabowo has set ambitious goals to boost economic growth to 8 per cent from the current 5 per cent.

Last year, Prabowo also removed fiscally conservative finance minister Sri Mulyani Indrawati and replaced her with the more growth-focused Purbaya, threatening the strict budgetary discipline that has been in place since the Asian financial crisis.

“[Indonesia] behaves like a frontier market,” said Charlie Linton, an Asia-Pacific portfolio manager at the Ninety One fund. “You’ve just had this undermining of institutions.”

Even doubled, the minimum for free floats remains below the 25 per cent usually required by regulators in India and Hong Kong.

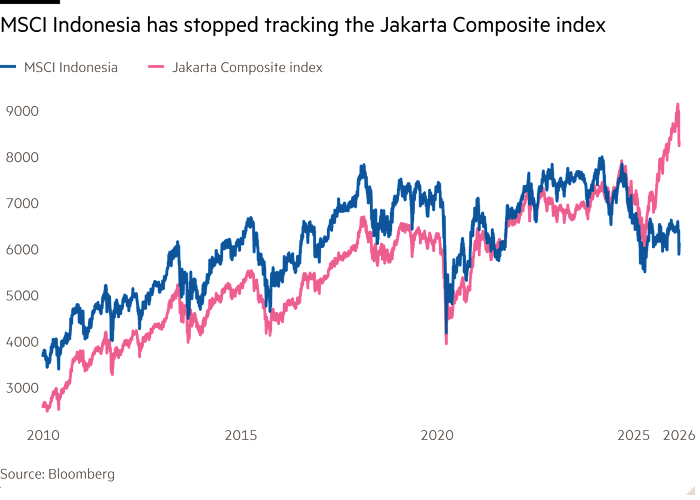

This has contributed to distortions in the market, investors say, as exemplified by the divergent performances of the MSCI Indonesia index, down 3.6 per cent last year, and the Jakarta Composite index, which was up 20.7 per cent last year. This was the largest deviation on record.

Investors say the market is split between stocks that are widely held by international investors and covered by analysts, such as banks, and a group of closely-held tycoon-owned companies that have on paper massively outperformed them.

Although other Asian emerging markets have similarly low trading volumes in certain companies, the problem is more severe in Indonesia.

“What has set Indonesia apart is the magnitude of what is happening,” said Yi Ping Liao, an emerging markets portfolio manager at Templeton Global Investments. “It’s much more significant than [in] any other Asian market.”

In recent years, investors say the problem has been exacerbated by the listing of large domestic businesses with relatively small free floats.

Among them are companies owned by Prajogo Pangestu, one of Indonesia’s wealthiest men. He controls 71 per cent of Barito Pacific, an industrial conglomerate listed in the 1990s, and almost 85 per cent of Petrindo Jaya Kreasi, a vehicle for mining interests listed in 2023. The latter’s shares almost quadrupled in price soon after listing. Even after the recent sell-off, the shares are up almost 50 per cent since the start of 2025.

Barito Renewables Energy, the conglomerate’s green energy arm also listed in 2023, also still has a dollar market capitalisation of $80bn, making it one of the biggest companies on the Jakarta index, but with a free float of just 12 per cent.

In 2024, FTSE, another index provider, deleted Barito Renewables Energy — 65 per cent owned by Barito Pacific — from its indices due to “high shareholder concentration”. Four shareholders controlled 97 per cent of the total shares of the company, FTSE said.

Barito Renewables Energy had then said it would monitor compliance with the Indonesian exchange’s free-float rules. “We are closely monitoring the situation and will await further regulatory guidance,” a spokesperson for Barito Pacific said on Monday.

Investors say the issues goes beyond free floats.

Companies such as Dian Swastatika Sentosa, controlled by the Widjaja family, also one of Indonesia’s richest, officially have free floats of 20 per cent, but investors say far fewer shares are available to trade because “friendly parties” hold those shares. The company did not respond to a request for comment.

In a statement to the FT, MSCI said it would “continue to monitor developments in the Indonesian market and engage with market participants and authorities, including the [financial services regulator] Otoritas Jasa Keuangan (OJK) and the Indonesia Stock Exchange (IDX), and will communicate further actions as warranted”.

Investors note that last year MSCI added some Barito group companies and Dian Swastatika Sentosa to its EM index despite their low free floats. MSCI did not respond a request for a comment about these additions.

“I think MSCI has done the right thing, and investors like us have been making comments to the Indonesian market authorities for some time,” said James Johnstone, co-head of emerging and frontier markets at investment manager Redwheel.

“There is almost a zero chance that Indonesia gets downgraded to frontier” given the market’s size, Johnstone said. But the MSCI warning was a “bold and dramatic” way to force a clean-up, he added.