Unlock the Editor’s Digest for free

Roula Khalaf, Editor of the FT, selects her favourite stories in this weekly newsletter.

Stefan Angrick is a senior economist at Moody’s Analytics.

Few things bring Bank of Japan-watchers more pure joy than speculating about the intricacies of the central bank’s policy framework and any changes that might be coming.

Whether it’s tweaks to “yield-curve control”, minor changes to the esoteric wording of policy statements, or shifts in the mechanics of the negative interest rate policy, timing the BoJ’s next move has become a favourite pastime for sellside analysts.

But how much do more casual observers actually need to care? Much less than you’d think!

Of the many levers at the BoJ’s disposal, adjustments to yield-curve control and negative interest rate policy would seem to be the most important. Both appear to be on their way out. And some people are naturally getting excited.

Alphaville reported yesterday how some investors are betting it will supercharge the wilting yen, but many think this might even be a big deal elsewhere too. From Bloomberg earlier this week:

What the BOJ does, and when it does it, will reverberate through world markets. The biggest consequence, according to MLIV Pulse respondents: more turbulence for the vast amount of Treasuries. That’s because higher yields in Japan would encourage fund repatriation by Japanese investors whose huge holdings include US, European and Australian debt.

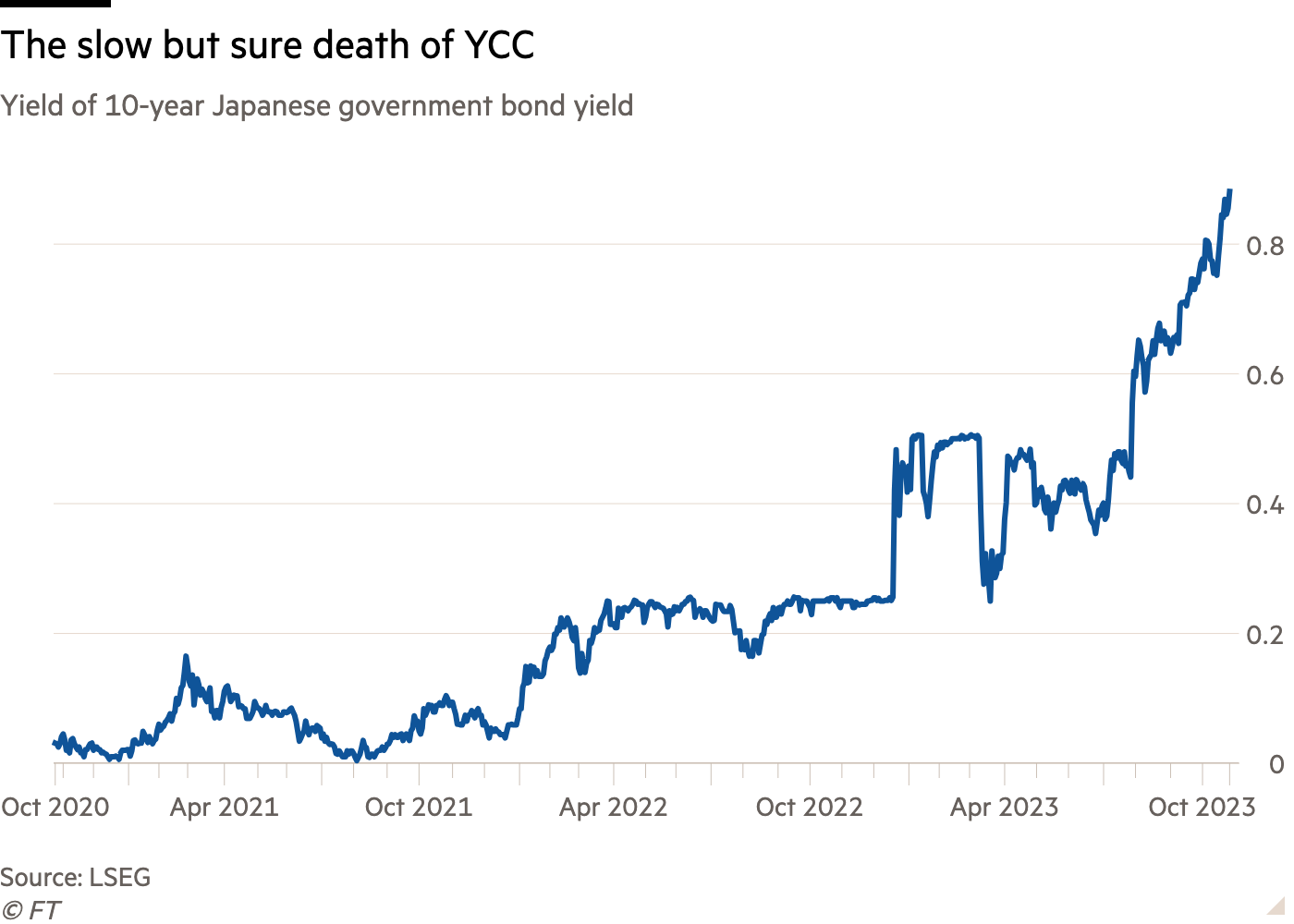

Although the BoJ’s official position is that it’s committed to easing, in practice it’s already been gradually dialling back support.

Borrowing costs for households and businesses have gone up after the BoJ widened the corridor around the 0 per cent target for 10-year Japanese government yields twice this past year. And the central bank’s increased focus on bond market functioning betrays some fundamental unease with the notion of capping long-term rates.

Meanwhile, subtle shifts in communication are laying the groundwork for a departure from negative interest rate policy. Recent BoJ reports have been going out of their way to stress the good news — better exports and the biggest pay gains in decades — while avoiding the bad — shrinking domestic demand and falling real wages.

Governor Ueda’s suggestion that the BoJ might have enough data by year-end to scrap negative rates also breaks with the past in an important way: Where the BoJ used to insist that sustained, robust wage growth was a prerequisite for rate hikes, it’s now putting that option on the table before results for 2024’s spring wage negotiations are known. This adds to the impression that negative rates will eventually get axed regardless.

And yet! The end of YCC and negative rates may inspire some to break out the champagne (or freak out for that matter) but in the grand scheme of things neither is terribly important.

Dropping YCC would simply eliminate what has by now become a fairly modest commitment to the 0 per cent yield target. Even without a formal peg, the BoJ would maintain some form of quantitative easing to limit government bond market volatility. More importantly, though, Japanese government bond yields just don’t have very far to go.

Even without YCC, the 10-year JGB yields would probably top out at 1 per cent. Other estimates might put yields a bit higher or a bit lower, but what they all have in common is that they’re not too far from the 0.85 per cent rate 10-year JGBs are trading at now.

Achieving a higher equilibrium rate, the infamous ‘R-star’, would require stronger productivity growth or inflation than seem plausible in Japan.

Yes, Japan’s challenging demographics raise the importance of productivity gains. But barring a significant acceleration in capex spending — which we haven’t seen yet — this can only go so far.

Meanwhile, inflation may in the future well run higher than in the past as geopolitical tensions reshape supply chains and climate change-related disruptions to food production become more common. But it’s important to keep things in perspective: Japanese consumer price inflation, excluding the impact of consumption tax hikes, has averaged a meagre 0.3 per cent annually in the decade prior to the pandemic. Even an increase to a new long-run average of 0.5-1 per cent would be a significant change.

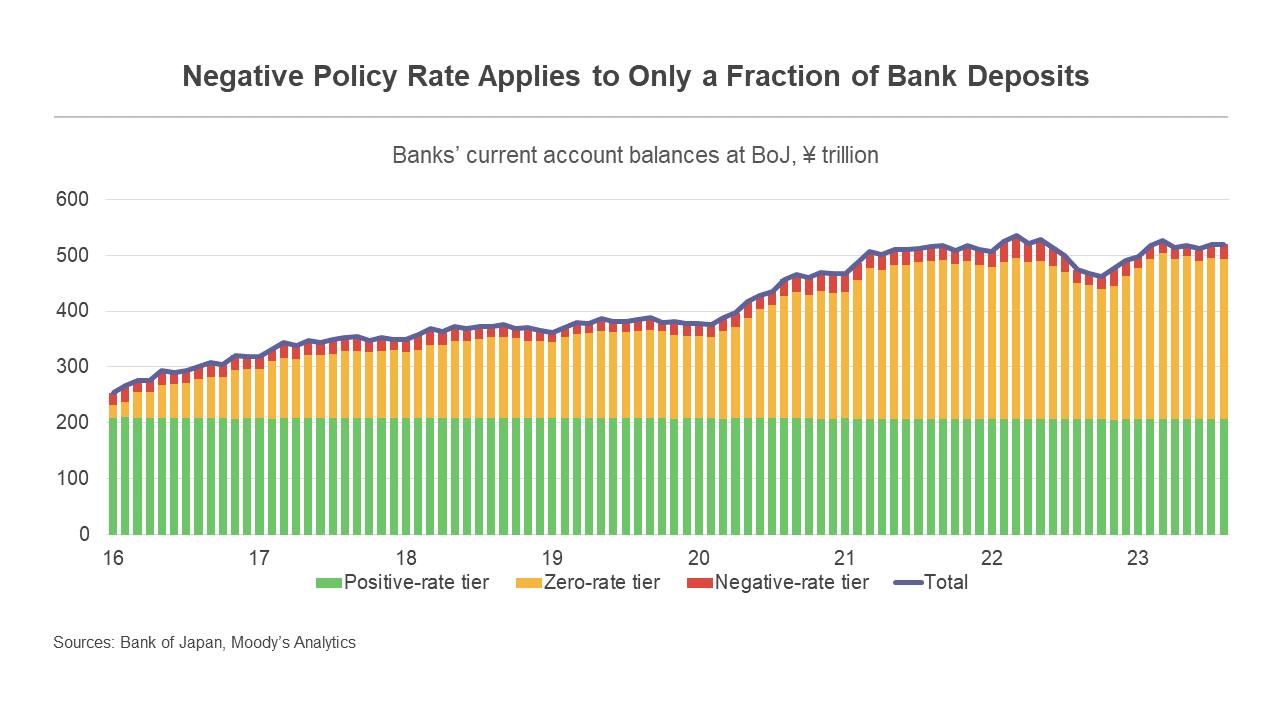

On the short end of the Japanese yield curve, it’s the tiering system that scrambles the economic calculus.

When the BoJ introduced negative interest rate policy in 2016, it split banks’ deposits at the central bank into three tiers, of which only the smallest is subject to the negative 0.1 per cent policy rate. The other two tiers are paid 0 per cent and 0.1 per cent interest.

This set-up ensures that the average deposit rate stays above zero, guaranteeing banks a positive amount of interest income which was intended to make the whole exercise more palatable (not that it had much success at that).

If negative interest rates were to be dropped, so would tiering. The BoJ would raise its short-term policy rate to 0 per cent, which matters to the overall optics of its policy stance. But banks would lose interest income from the tiering. So fundamentally things wouldn’t change very much.

This is also what makes it such an attractive policy option. Returning to zero rates and quantitative easing would make the BoJ’s policy setting a tad more conventional (now there’s a word that rarely shows up in the same sentence as ‘quantitative easing’) without changing the substance too much.

So, while it’s fun to speculate about when and how YCC and negative rates might get axed, don’t expect fireworks.