This article is an on-site version of our Unhedged newsletter. Sign up here to get the newsletter sent straight to your inbox every weekday

Good morning. Microsoft delighted and Alphabet disappointed in earnings yesterday. Competition in the cloud appeared to make the difference. Google Cloud sales, despite growing 22 per cent, missed analyst expectations by 3 per cent, while Microsoft’s Intelligent Cloud beat expectations by 3 per cent. Microsoft stock rose 3 per cent and Alphabet fell 7 per cent after hours, a reminder that the “magnificent seven” stocks rely on magnificent results. Email us: robert.armstrong@ft.com and ethan.wu@ft.com.

China: OK growth meets property tail risks

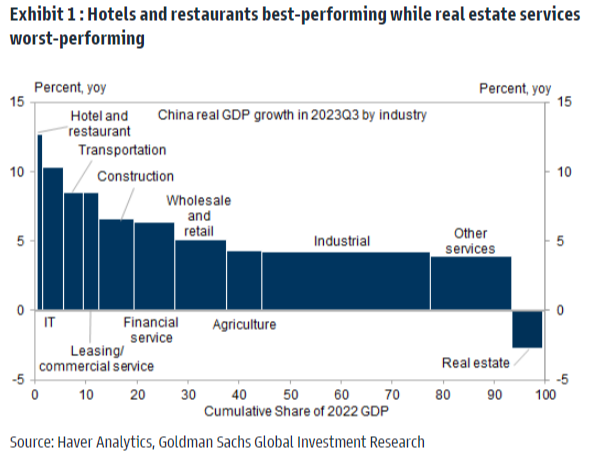

While China’s property sector remains in crisis, its business cycle seems to have stabilised. Some of the deep gloom of July has worn off as retail sales, fixed-asset investment and industrial production all improve. As hyper-cautious consumers get a bit more confident, the household savings rate has fallen (though it is still high). China looks likely to meet its 5 per cent growth target this year; it will almost certainly come close. The chart of third-quarter GDP below from Goldman Sachs sums up the picture:

But this set-up — cyclical moderation paired with an unresolved structural meltdown in property — has not reassured markets. The CSI 300 on Monday fell to pre-pandemic levels. Chinese stocks are down 40 per cent from their 2021 peak and 11 per cent this year. Comparisons to the S&P 500, or the Topix, or EM ex-China indices look ugly. The Financial Times’ Hudson Lockett and Cheng Leng included this quote in their story on Monday:

“Global investors need two floors before they get back into China — they need a floor for the geopolitics and a floor for the Chinese economy,” said an Asia-based senior capital markets banker at one Wall Street investment bank. “Only then they can start pricing things up.”

There is too much tail risk, in other words, overwhelming any nascent hype about China’s “new three” sectors (batteries, EVs and renewables).

One tail-risk scenario looms large: heavily indebted local government financing vehicles inflicting losses on Chinese banks. LGFVs are shell companies local governments use to borrow for land development and infrastructure spending. Nearly a third of LGFVs have interest coverage ratios below 1 (ie, ebitda < interest expense). And China’s banks, which own 80 per cent of LGFV debt, already have relatively thin equity buffers. If things get gnarly, the central government would intervene, of course. But the state is constrained by fears of worsening moral hazard, and by its desire to curb over-indebtedness. So there remains scope for, say, a crisis of confidence that runs out of the authorities’ control. A recent IMF modelling exercise lays bare the risk to smaller Chinese banks:

If all LGFVs were restructured to ensure financial viability (with current earnings covering interest expenses), losses would be large. If banks were to take half of the responsibility of the debt restructuring cost, they could face impairment charges of about 3.4 trillion yuan, equivalent to a reduction in capital ratios of 1.7 percentage points. Although systemically important banks would be able to manage, local banks could face capital shortfalls, even in relatively fiscally healthy provinces

Sizing up the risks here is hard, because so much depends on central government decision-making, which is opaque (to us anyway). But we can look at what the state can, and has, done to guard against a financial crisis.

The most obvious is a dose of fiscal stimulus. Yesterday, China announced just this. The state approved Rmb1tn ($137bn) in central government bond issuance, worth a bit less than 1 per cent of GDP, with funds transferred directly to local governments for use on infrastructure in areas hit by natural disasters. This alone is not big enough to fix local government finances, but on the margin, it should lower their average funding costs.

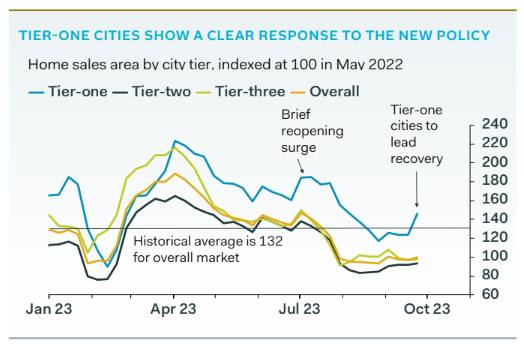

Another option is targeted, but limited, support for the property market. The state is trying. Average mortgage costs are near an all-time low, down payment requirements have been eased, and restrictions on second home purchases lifted. This is having at least some effect. Home sales in major “tier one” cities have started rising (chart by Duncan Wrigley of Pantheon Macroeconomics):

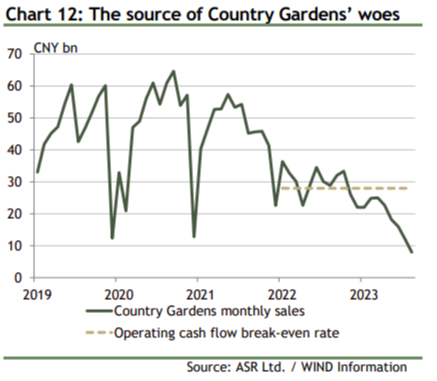

More may be needed. Tier-one cities make up just 5 per cent of sales volume. Adam Wolfe, EM economist at Absolute Strategy Research, estimates in a recent note that authorities need to raise annual property sales by about 15 per cent to stabilise the sector. That would address what he sees as the underlying problem: property sales have fallen too far, too fast. Even a modest improvement in sales would let developers unload inventories and continue servicing debts, limiting losses to the banking sector. Wolfe gives the example of the all-but-defaulted Country Garden, which managed to survive the first sales plunge, but not the second:

Some good old-fashioned extend-and-pretend tactics are probably needed, too. Refinancing LGFV debt would deprive banks of interest income, but put off the far scarier prospect of big loan losses. As Reuters reported last week, China’s central bank has told state-owned banks to stretch out LGFV debt at lower rates, and not to classify certain loans as non-performing. Other efforts at refinancing are under way: Goldman counts nearly Rmb1tn in special refinancing bonds issued by local governments this year. The state-led push to restructure local government finances has even sparked an LGFV bond rally.

In sum, China is not sitting idly by while the financial system creaks. But the deeper constraints, an aversion to moral hazard and an ambition to curb debt, still bind. Just how the state strikes the balance is crucial. And that poses a problem for markets. China investors want tail risks eliminated as soon as possible. But the state may take its time. (Ethan Wu)

Stock pickers do not pick stock pickers’ stocks

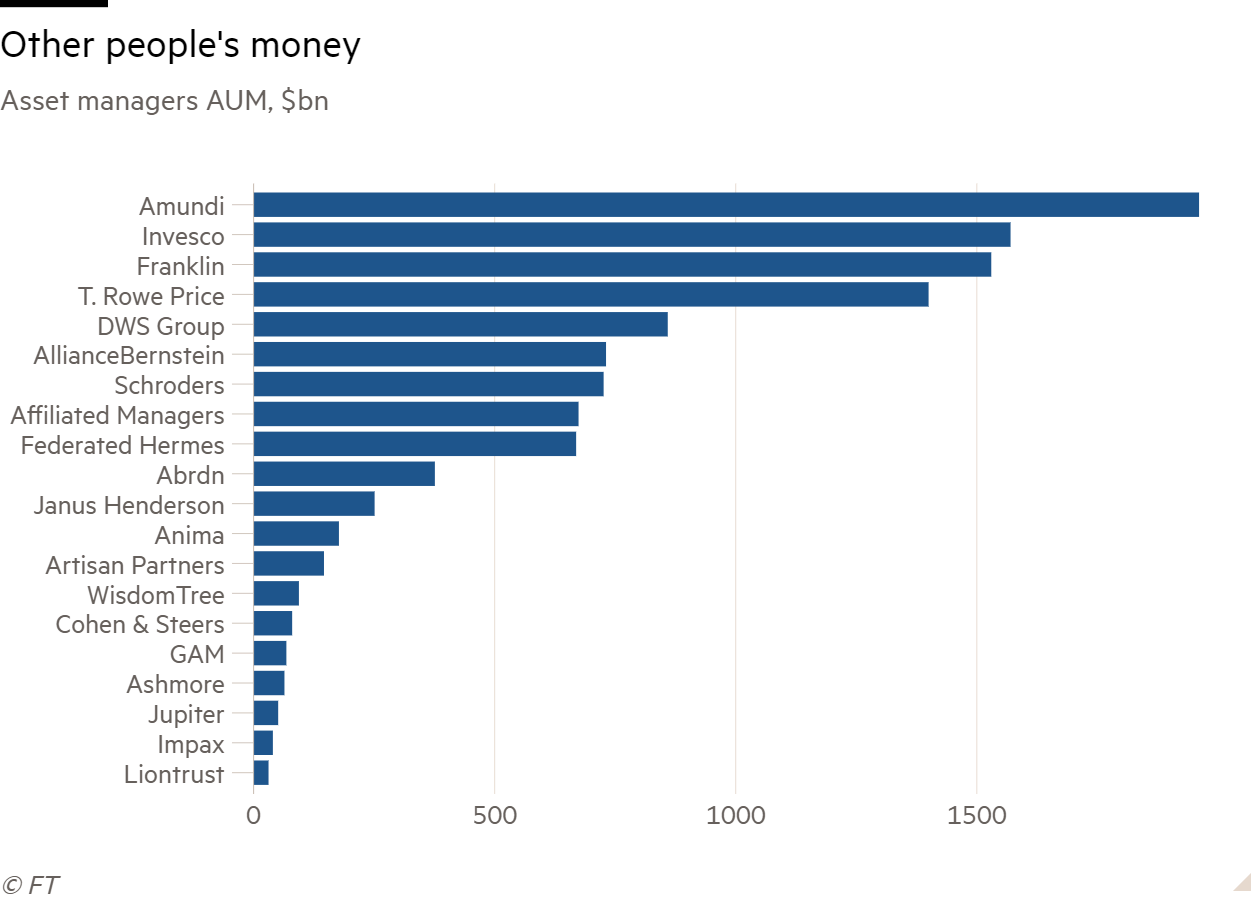

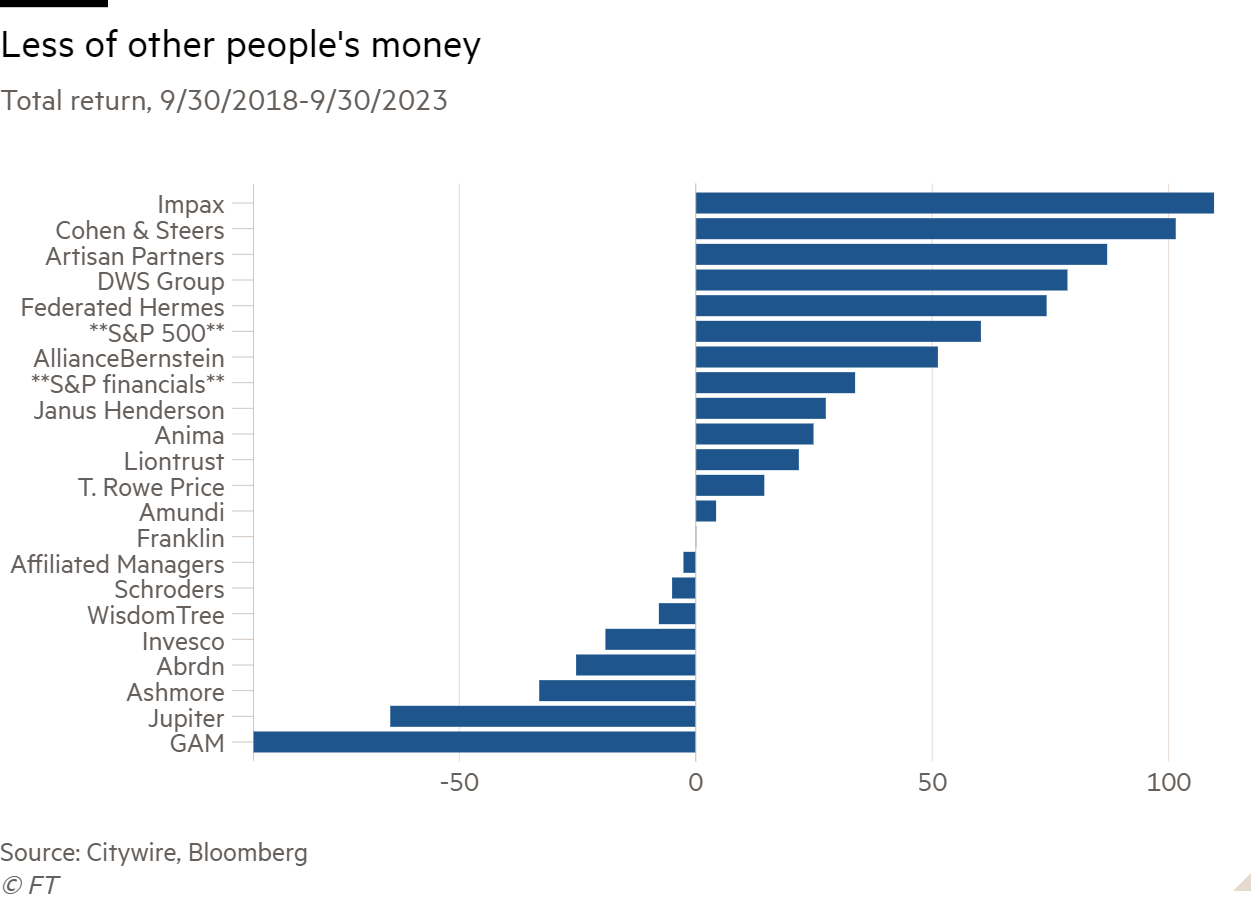

In response to yesterday’s column about secular decline in the fund management industry, I received an email from Richard Lander of Citywire, which covers the industry very closely. He pointed out, first, that the performance of a larger sample of long-only asset managers was just as bad as the sample of five large ones I talked about yesterday. The top 20 publicly traded asset managers by assets under management, excluding the private equity monsters like KKR and the passive giant BlackRock, have notched an average cumulative total return of 17 per cent over five years, trailing both the S&P 500 (60 per cent) and S&P financials companies (34 per cent). Here is the sample, along with their AUMs:

And here are their total returns:

Notably, all of the positive returns for the group, and more, come from dividends. Average price return was negative 9 per cent. Wisely for a declining industry, the fund managers are pushing cash out the door.

Even more interestingly, Citywire’s Daniel Grote pointed out that the best portfolio managers do not tend to invest in fund managers’ shares. Citywire rates companies based on their popularity with top-performing managers (it tracks more than 10,000 equity fund managers worldwide). Of the 329 highest-ranking fund managers, only 44 have any position at all in the shares of the traditional, long-only asset managers; only 36 are overweight. That is very low, Grote says, even for a niche industry. Grote makes the comparison, to say, healthcare plans: 81 top managers are invested. Stock pickers don’t pick stock pickers. In Lander’s words, “it doesn’t get more meta than that”.

Errata

Monday’s newsletter contained a bad typo and an outright error. The direction of Fed policy was therefore misrepresented, and the meaning of the term premium was jumbled. Both have been corrected in the web version. Unhedged feels dumb and will endeavour to do better.

One good read

The corporate retreat from Hong Kong.

FT Unhedged podcast

Can’t get enough of Unhedged? Listen to our new podcast, hosted by Ethan Wu and Katie Martin, for a 15-minute dive into the latest markets news and financial headlines, twice a week. Catch up on past editions of the newsletter here.