Weekends are when Stacy Wang makes the best of her new home. A native of Beijing, the 42-year-old moved with her young son to Kowloon, just over the water from Hong Kong Island, to join her husband, who was posted there by his mainland-based company. Together they arrange play dates in the Kowloon Cultural District, spending time in the park or visiting the science and space museums. Now that temperatures are milder, they hike up The Peak or walk around Upper Shing Mun Reservoir; her son loves the wild monkeys. Their rental building offers facilities she would not have had back home, including a pool, gym and clubhouse. And she is released from wider family obligations. “Here all we have to do is plan for the weekend,” she says.

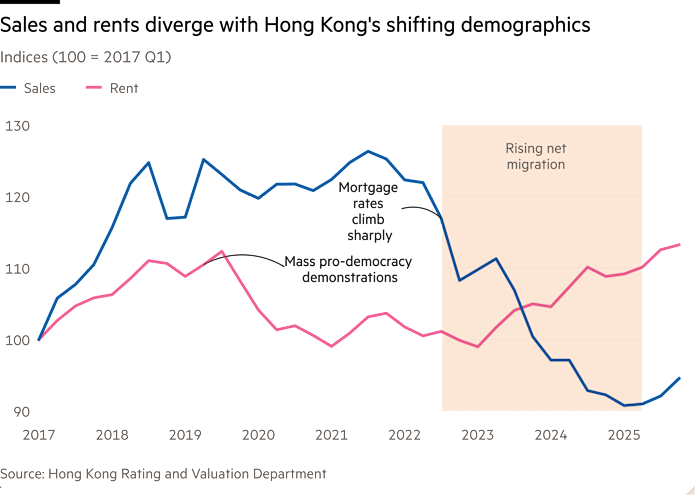

Such draws are luring many mainland Chinese to Hong Kong. In the three years to June 2025, there were 206,000 net new arrivals to the special administrative region, which includes Hong Kong Island, Kowloon and the New Territories; the largest group have been mainlanders arriving to work or study. The surge has driven up median rents by 16 per cent since mid-2022 to close to record levels, and tightened supply across the city. Mandarin is increasingly heard alongside local Cantonese, while many bars and restaurants are quieter as closer ties to the mainland encourage residents to travel north for cheaper shopping and eating. Today, most new arrivals still rent. If they settle and buy homes, Hong Kong’s sales market, where prices are 25 per cent below their 2021 peak, will receive a much-needed boost.

The recent influx follows an exodus that reshaped the housing market in Hong Kong. Roughly 170,000 more people left the city than arrived in the two years to June 2022, as the aftermath of the 2019 pro-democracy protests and a new national security law in June 2020 raised concerns about tightening political controls, curtailing civil liberties and Hong Kong’s future autonomy. Many were expatriates; many others were wealthy local families who sold homes. But since 2023 the flow has reversed.

Part of the appeal is Hong Kong’s booming financial sector. It led the world in total value of IPOs last year and its stock market returned 27 per cent, its best performance since 2017. This time, however, Hong Kong’s recovery is a comeback with Chinese characteristics. Recent IPOs have been dominated by mainland companies raising capital offshore; many are underwritten by mainland banks, with large Chinese workforces.

The shift is already changing estate agent strategies — even international firms have tilted sharply towards mainland demand. “Probably 50 per cent of our rental business used to be expatriates from countries like the UK, the US and Europe. Today it’s closer to 20 per cent,” says Frank Marriott, head of regional investment advisory for Savills in Hong Kong.

Senior mainland executives or entrepreneurs and wealthy Chinese relocating to Hong Kong with their families, including for schooling, dominate the super-prime market. “While we don’t observe any significant surge in rents [these groups] more than compensate for the void created by western expatriates [leaving],” says Samson Law, executive director for Christie’s International Real Estate in Hong Kong. According to Christie’s, the most expensive homes — renting for more than HK$500,000 ($65,000) per month — typically transact off market, such is the current level of demand.

Besides the financial incentives, they are seeking the city’s lifestyle benefits — including 85 international schools, roughly equivalent to Shanghai and Beijing combined, and more than double the number of Michelin-starred restaurants of Shanghai or Shenzhen. “Many [mainlanders in Hong Kong] view it as their stepping stone for primary and secondary education, before university in the west,” says Law. A recent Savills survey, which assessed factors including business environment, lifestyle and the ease with which wealth can be passed between generations, ranked Hong Kong the fourth most appealing city globally for the world’s wealthiest individuals.

Hong Kong’s residency-by-investment programme, suspended in 2015, was retooled and relaunched in March 2024: today, those investing at least HK$30mn into approved assets — including up to HK$10mn in a qualifying HK$30mn-plus home purchase — receive residency for an initial period of two years. “This certainly attracted a number of high-net-worth individuals. The favourable tax conditions are another reason,” says Martin Wong, head of research and consultancy for greater China at Knight Frank, citing Hong Kong’s low income tax and zero tax on capital gains and inheritance.

New arrivals are by no means limited to senior executives or entrepreneurs, however. Benjamin Quinlan, 42, the Hong Kong-born founder of local strategy consulting company Quinlan Associates, sees it in new hires. Until recently, he recruited one graduate or junior consultant a year from a shortlist of one or two. Last year, he had six standout applicants and hired two. The difference was the Top Talent Pass Scheme, a visa programme introduced in 2022 that includes fast-track access for graduates from the world’s top 100 universities; it has approved about 109,000 applications so far. “It’s just much easier to source global talent now,” he says.

Nor are all of Hong Kong’s new residents from mainland China. One senior colleague of Quinlan’s who moved to Singapore in 2020 to avoid Hong Kong’s tight travel restrictions during Covid has just moved back. When Quinlan and I speak, he has just returned from a lunch with two newly arrived partners at a Big Four consulting company — one Scottish, the other Australian.

When it comes to finding a rental home, young skilled professionals jostle with a fast-expanding crop of those arriving for university. Annual foreign student enrolments at Hong Kong universities have doubled over the past five years to about 92,000, and at the eight largest publicly funded institutions, around 80 per cent of foreign students are now from the mainland. “Self-financing postgraduate students are increasingly driving demand in mid to lower-tier rental housing: a typical two or three-bed rental home — sought by three or four students — costs between HK$15,000 and HK$25,000,” says Wong.

Moving from the mainland provides other challenges, too. A few days after she arrived, Wang took a local minibus with her son to go shopping in Kowloon. The 15 to 20-seat vehicles, in which passengers typically shout their stops in Cantonese to a driver weaving at hair-raising speed through city traffic, are a staple of Hong Kong life. But Wang spoke only Mandarin: she could not communicate her stop to the driver.

The streets were unfamiliar, a blur of neon-lit wet markets and noodle shops; the taxis, minibuses and buses jostling for space on narrow congested roads, hemmed by bamboo-scaffolded buildings and cranes assembling new residential towers, with the distinctive Hong Kong Island skyline rising into cloud across the harbour. She had no way to recognise her destination when it came into view. “I was about to end up lost in a city I didn’t know, whose inhabitants didn’t understand me,” she tells me, in English.

The city’s record IPO market is not the only way Hong Kong’s closer ties to the mainland are leaving a mark on the island. In Lan Kwai Fong and Wan Chai, where popular bars once swelled with international expat financiers, lawyers and accountants spilling out on to the steep streets after work, business is markedly quieter. A high-speed rail connection links West Kowloon station to Shenzhen North in 15 to 20 minutes; more Hong Kong residents are lured to the mainland’s cheaper shops, bars and restaurants. “Lots of people do their shopping there. Hong Kong can’t compete on price with the mainland on day-to-day things,” says Quinlan.

Meanwhile, the question is whether Hong Kong’s home sales market can recover from its current funk. This will take returning confidence from local and mainland buyers and a choice by many of the new arrivals to buy homes.

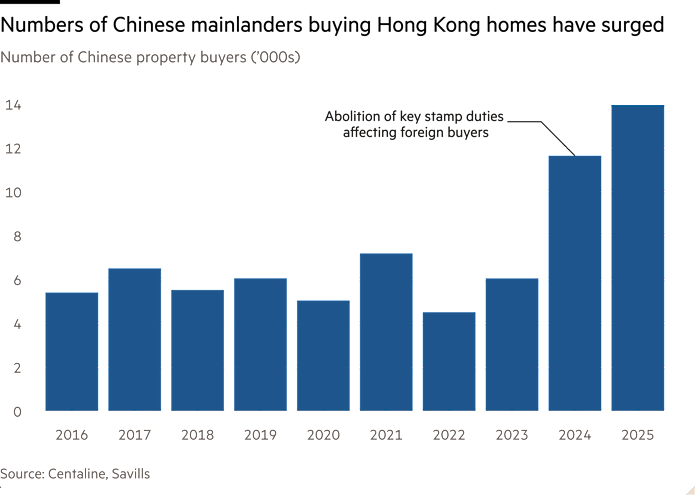

Mainland buyer purchases more than doubled from 6,000 in 2023 to 14,000 in 2025, according to data from Savills and Centaline, helped by the removal in February 2024 of the 15 per cent foreign buyer tax and the 15 per cent second home tax (paid by both foreign and domestic buyers).

China’s own property downturn, meanwhile, has been a mixed blessing for Hong Kong. Since 2021, defaults of major developers such as Evergrande, unfinished homes and falling prices on the mainland have dented confidence. The relative appeal of Hong Kong has increased. “This is both as a store of wealth and a marker of status. It offers a transparent legal framework, deep capital markets and currency stability via the US dollar peg,” notes Woody Mah of List Sotheby’s International Realty in Hong Kong.

However, the mainland property market slump has spilled over to Hong Kong. Chinese banks have forced failing mainland property companies with Hong Kong developments — and some of China’s super-rich — to sell homes at steep discounts. Last year produced a series of striking fire sales. 15 Gough Hill Road is an 18,000 sq foot house on The Peak, the hilltop neighbourhood of sprawling mansions and trophy apartment blocks. It was bought in 2016 by mainland property tycoon Chen Hongtian for HK$2.1bn (US$315mn at the time) before being sold by receivers in August 2025 for HK$790mn, when Hongtian’s business, which included assets he had used to secure loans to buy the home, missed loan repayments. In April, Gale Well Group, a Hong Kong developer, sold an apartment at Hong Kong Parkview in Tai Tam, on the island’s south-east side, for HK$138mn, having first listed it at HK$200mn — one of several steeply discounted sales by the company.

Marriott expects more super-prime homes to come to market this year. In The Peak, where around eight homes typically change hands in a year, more than 90 properties are currently listed. Sotheby’s is selling a four-bedroom town house with harbour views and a garden in the Severn Hill development, for HK$190mn. In nearby Watford Road, Knight Frank is selling a town house,with a garden for HK$128mn; a four-bedroom town house on Plunkett’s Road is for sale with Christie’s for HK$470mn.

Step into the broader prime market and the picture is similar: at current sales levels, the inventory of unsold town houses and luxury apartments will take more than 10 years to clear, according to Savills. Across the wider market, around 101,000 homes are for sale or due for completion over the next two years, an overhang the agency estimates will take about five years to clear.

Helped by falling mortgage rates, some buyers believe now is the time to take advantage of low prices. Last autumn, Quinlan bought a house for his family, the second such purchase in three years. He has kept the previous home, adding it to a growing rental portfolio to take advantage of rising rents. This time he fixed his mortgage for five years at 2.71 per cent with HSBC. “I would have got roughly 4 per cent a year ago,” he says.

Jonathan (who prefers not to use his real name) is originally from the UK and has rented for the past 20 years in Hong Kong, where he owns and runs an investment management company. He recently took advantage of low prices — and the same mortgage rate with HSBC as Quinlan — to buy a town house with his wife on the south of the island for 10 per cent less than the list price, which the couple intend to renovate. “We plan to be here for many years; Hong Kong always bounces back,” he says.

Price cuts like that of Gough Road have boosted sales of the territory’s most expensive homes: 81 sold for more than US$10mn in the final quarter of last year, according to Knight Frank — the most in any global city other than Dubai — bringing the 2025 total to 232, up from 166 a year earlier. In December, Hong Kong conglomerate Swires sold two three-storey homes on a single lot, on Deep Water Bay Road, part of Hong Kong’s super-prime southern coastal belt, for HK$2.2bn. “The repricing has reset expectations and restored confidence,” posits Mah.

On February 26, Hong Kong’s government hiked stamp duty charged on homes sold for more than HK$100mn from 4.25 per cent to 6.5 per cent. Eighty per cent of these homes are bought by mainland Chinese, according to Mah; the extra cost will be “marginal relative to the strategic and lifestyle motivations behind these acquisitions”, he believes.

House & Home Unlocked

Don’t miss our weekly newsletter, an inspiring, informative edit of the news and trends in global property, interiors, architecture and gardens. Sign up here.

Across the market as a whole, prices gained 3.9 per cent in the nine months to December, compared with one year earlier, according to government data; the most sustained recovery since early 2019. But whether new arrivals will purchase homes and sustain a lasting recovery is hard to say. Most rent initially, reiterates Wong: “They’d rather settle and understand the geography before purchasing.” A February Goldman Sachs report suggested that strong rental price growth and lower mortgage rates could push many renters to make a purchase; it forecast price growth this year of 12 per cent. But prospects for visa extensions, perceived job stability and whether families of recent arrivals want to join them are difficult variables to predict.

Wang has not made up her mind about whether to stay and invest in a home. With her son settled at school she worries about returning him to Beijing. But she says she still feels “an outsider” in her new home — without Cantonese, she misses the rapport she enjoyed with locals in Beijing. Meanwhile, her husband’s employer pays for the rent on the family’s apartment in Kowloon, protecting them from rising rental prices; for now the couple have no intention to buy. “I would be happy to live here for a longer time, but we don’t have a solid plan,” she says.

Find out about our latest stories first — follow @ft_houseandhome on Instagram