Good morning. The war has escalated with both Israel and Iran hitting oil and gas reserves in the Middle East. This, added to the Federal Reserve’s decision to hold US interest rates, caused Indian stock markets to plunge on Thursday, with the benchmark indices posting losses of more than 3.2 per cent. The other big business news came from the country’s biggest private lender, HDFC Bank, where part-time chair and independent director Atanu Chakraborty tendered his resignation rather abruptly, citing ethical differences.

Adani takes home the prize

In the battle of the billionaires for a debt-laden company, Gautam Adani has this week emerged victorious over Anil Agarwal.

The company in question is Jaiprakash Associates (JAL), which has several attractive assets, including a vast land bank, despite debts of Rs550bn ($5.9bn). In November, JAL’s creditors chose a bid by Adani Enterprises to acquire the company despite a larger Rs170bn offer by Agarwal’s group Vedanta. The committee of creditors — which included the State Bank of India, the country’s biggest public lender — said Adani’s proposal offered better terms, including a higher upfront payment. Vedanta had countered by raising the amount it was willing to foot upfront, but the move was dismissed by creditors on the grounds that they could not extend special treatment to any particular bidder. A person close to the proceedings told me Adani’s proposal secured 93 per cent of the votes.

Last month, Vedanta challenged the decision with the National Company Law Tribunal, but the NCLT on Wednesday ruled in favour of Adani. Vedanta has the option to appeal against the decision. I reached out to the company for their comments but they have not responded to my email.

As is often the case in such proceedings, ordinary investors are the worst affected. A stock exchange filing by JAL says equity is to be extinguished without any compensation, which means shareholders will be left with nothing. Even creditors are expected to recover less than 3 per cent of their total claims.

While JAL’s rise and fall offers several cautionary lessons, the more troubling questions are about the effectiveness and timeliness of insolvency proceedings in India as a whole. The rules of engagement often appear to shift, creating uncertainty. Several cases under the Insolvency and Bankruptcy Code have been marred by prolonged litigation and repeated challenges.

Perhaps the most striking example was the Supreme Court’s order last year nullifying JSW Steel’s acquisition of Bhushan Power & Steel — four years after the deal had been considered complete. Although the court later reversed its decision, the episode underscored the unpredictability of insolvency proceedings in India. They are never truly over until they are over — and, sometimes, not even then.

Do you think the creditors were right to pick Adani’s proposal over that of Vedanta? Hit reply or email me at indiabrief@ft.com

Recommended stories

The Reserve Bank of India is battling to protect the rupee from Iran war fallout.

Iran, which has set its price to end the war, is allowing a handful of favoured ships through Strait of Hormuz.

The AI craze, Open Claw, has taken Chinese users by storm.

Microsoft weighs legal action over $50bn Amazon-OpenAI cloud deal.

How can we tell good AI from bad?

Meet Roy Chan, Hollywood’s hottest A-list trainer.

Young and jobless

Almost 40 per cent of Indian graduates are unemployed, research shows — a rate that has remained stubbornly unchanged for more than four decades.

A report by Azim Premji University shows that the share of graduates aged under 25 who are unemployed has stayed the same since 1983. This suggests that India faces structural problems in entry-level hiring that it has not been able to resolve. What makes the situation worse is that the number of graduates is increasing rapidly, adding to the absolute number of unemployed graduates. About 5mn Indians now complete formal higher education every year.

All of this raises a critical question: will India be able to fully capitalise on its demographic dividend, which has been a cornerstone of its growth narrative over the past two decades?

Job prospects seem to be only getting more challenging, as AI and other workplace automation make mass recruitments unnecessary. The IT sector, which has been a major source of white-collar employment in the past three decades, accounts for 13 per cent of jobs for male graduates and 18 per cent for female graduates. But large Indian technology companies are now scaling back on hiring due to technological disruption and geopolitical uncertainties affecting business prospects.

Another major concern is the quality of education and whether it produces employable graduates. While there has been a proliferation of new institutes and universities to cater to the educational needs of a growing population, their overall quality standards are questionable. A report by the Confederation of Indian Industry said only 46 per cent of Indian graduates were considered employable by industry standards, forcing companies to earmark substantial resources to upgrade their skills.

Alarmingly, successive governments have been unable to find a solution. India is now at the peak of its potential demographic dividend, and its share of the working-age population will begin to decline from 2030. An ageing population will place increasing pressure on a relatively smaller working population. Meeting the twin challenges of poor skills and poor employment cannot be delayed any longer.

Go figure

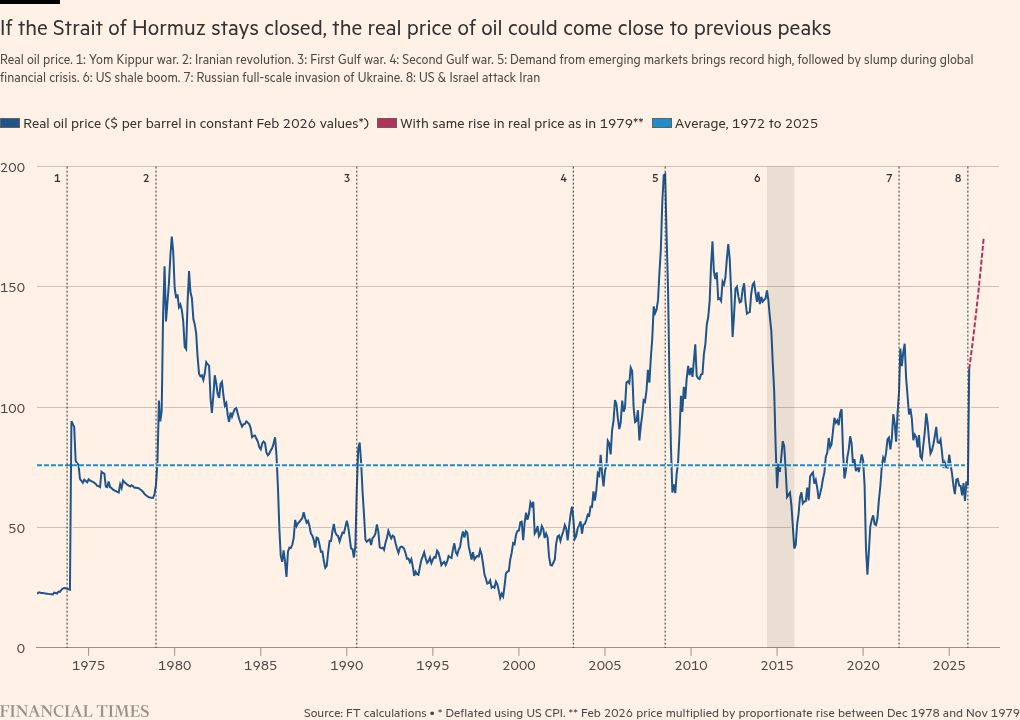

The war in the Middle East is creating the largest supply disruption in the history of the global oil market, according to the International Energy Agency. If the Strait of Hormuz stays closed, the real price of oil could come close to previous peaks. That and other truth bombs are addressed in this column by the FT’s Martin Wolf.

Read, hear, watch

I am reading Hotel Babylon, an hour-by-hour account of a day in the life of a top London hotel. Although tagged as fiction, it cuts pretty close to reality. The book is as engaging as it is horrifying.

I am totally sold on the idea of punting on babies, and am looking forward to playing Space Warlord Baby Trading Simulator. The premise reminded me of Bitlife, a game my daughter introduced me to, a hilarious life simulator in which you can determine the fate of the characters from birth to death. Why give up on an opportunity to play God?

Buzzer round

Which furry viral sensation has nine teeth, has collaborated with brands such as Uniqlo, Coca-Cola and Vans, and even has a movie being developed by Sony Pictures?

Send your answer to indiabrief@ft.com and check Tuesday’s newsletter to see if you were the first to get it right.

Quick answer

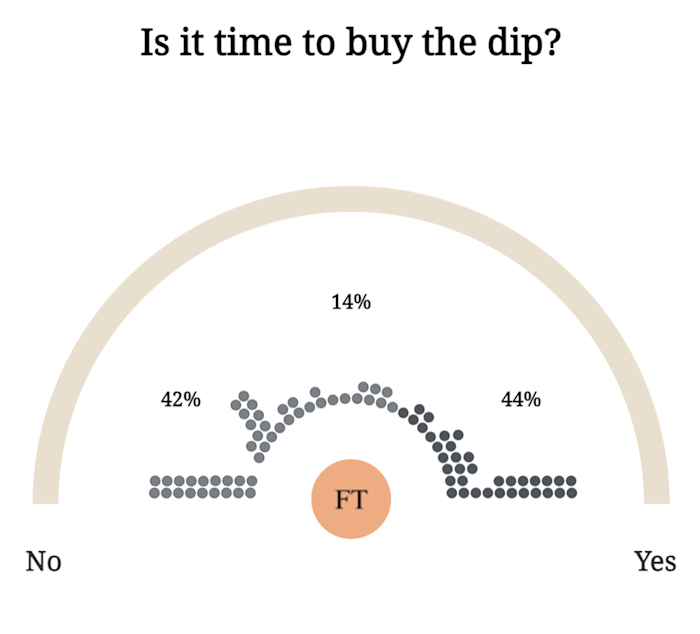

On Tuesday, we asked if it was time to buy the dip in the stock market. It’s a close one. I hope the 44 per cent of you who voted yes on Tuesday waited until Thursday to act on it. Here are the results.

Thank you for reading. India Business Briefing is edited by Tee Zhuo. Please send feedback, suggestions (and gossip) to indiabrief@ft.com.