Unlock the Editor’s Digest for free

Roula Khalaf, Editor of the FT, selects her favourite stories in this weekly newsletter.

The writer is Asia equity strategist at Société Générale

The past year has been transformative for Korea’s equity market. What began as a cyclical rebound in late 2024 rapidly evolved into one of the strongest global equity rallies of 2025.

The Kospi surged almost 80 per cent in 2025, with the momentum spilling into 2026 as the index rallied about another 50 per cent year‑to‑date. By early 2026, South Korea’s total market capitalisation had climbed high enough to surpass Germany and France, marking a symbolic elevation of the country within the global equity landscape. However, that was all before the correction of nearly 20 per cent over the past two days. The wild ride points to the strengths and weaknesses of this market.

South Korea has conventionally been a deeply cyclical Asian stock market, tightly wired to the global economic cycle. Its export‑led structure — dominated by semiconductors, autos, shipbuilding, defence and energy equipment — has always made it vulnerable to global demand swings.

Layered on top of this cyclicality is the longstanding “Korea discount”, rooted in concerns over corporate governance, limited minority‑shareholder rights and the influence of the chaebol, the big family-run conglomerates in the country. Over the past 15 years, the stocks of the benchmark Kospi index have traded at a modest average valuation of close to one times the book value of its assets, reflecting these structural concerns.

One of the most meaningful shifts over the past year has been the acceleration of corporate‑governance reforms under President Lee Jae‑myung, who also set high ambitions for the stock market known as the “Kospi 5000” plan. Elected last June, the administration has demonstrated a strong commitment to strengthening investor protections, improving capital efficiency and elevating Korea towards developed‑market status for index providers.

Central to this agenda is the “Value‑Up” programme, originally introduced under the previous government to close the Korea discount. Further reforms include more transparent disclosure standards, the reform of cross‑shareholding structures and requiring companies to cancel treasury shares after set periods rather than hold them to use to support company managements. The new administration has also focused on policies to strengthen domestic equity demand, including tax incentives for retail investors to buy domestic stocks.

The second major driver of Korea’s market repricing has been the unprecedented surge in demand for high‑bandwidth memory and AI‑infrastructure components. This reinforced Korea’s dominance in specialised memory and sparked a powerful earnings‑revision cycle. Tight supply, multiyear contracts and steep pricing gains created a self‑reinforcing loop of earnings upgrades, valuation expansion and index re-rating. As a result, Kospi stock valuations rose by more than 100 per cent to over two times price to book value at the recent peak.

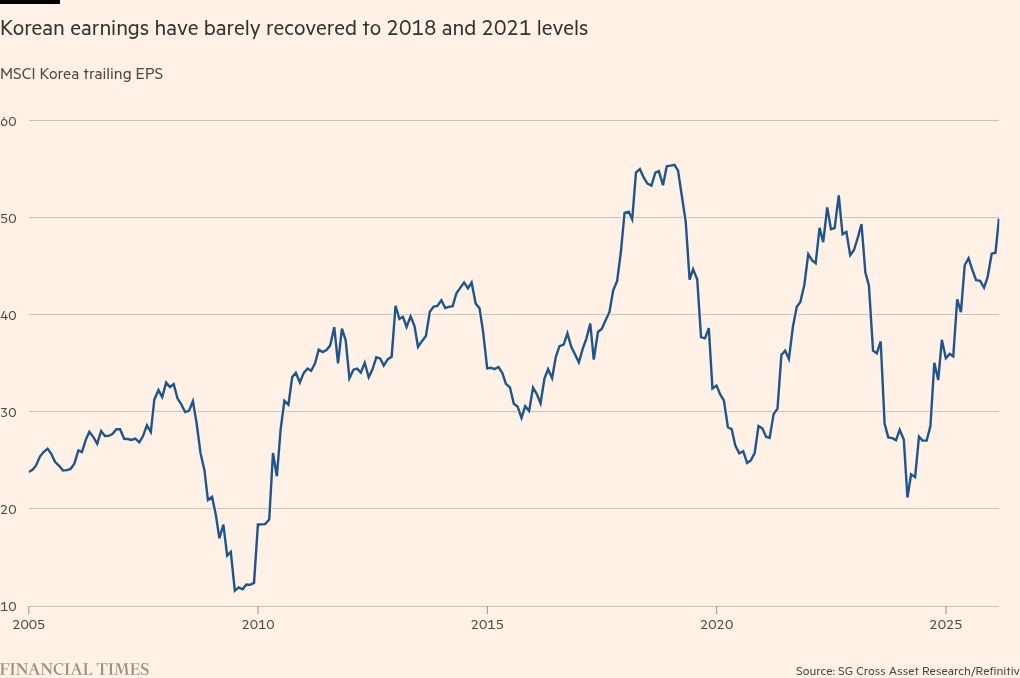

However, the core characteristics of the market are unchanged. Korea remains a narrow and top‑heavy market, dominated by the top five stocks, which account for more than half of the Kospi. This narrow leadership is mirrored in the earnings mix, with the semiconductor sector expected to contribute more than half of total earnings growth in 2026. The fact that trailing earnings per share for constituents of the MSCI Korea index struggled to break past previous cycle highs from 2018 and 2021 — even amid robust AI‑related growth — highlights the still‑volatile nature of Korea’s earnings structure.

Notably foreign investors, who were early buyers after the elections, have been consistent net sellers since November, withdrawing nearly $15bn this year. Retail investors, meanwhile, have been the most active buyers during sharp corrections, particularly in November, February and March, employing a “buy‑on‑dips” strategy.

The past year’s trajectory of Korean equities is a compelling illustration of market psychology, where buying begets buying until the laws of physics apply to markets: a body in motion continues to move until acted upon by an external force. For Korean equities, that external force came in the form of rising geopolitical tensions.

For now, the momentum has been broken. It typically takes time for the market to stabilise and form a durable base. In the near term, investors will become more watchful of fundamentals before returning to the market with the same fervour. However, this deep correction may also attract a new cohort of investors who had long been waiting for a meaningful pullback.