From the Port of Rotterdam to the retailer Superdrug, and from London’s electricity grid to the mobile network Three, one thing is clear: Li Ka-shing is not sentimental.

Hong Kong’s most prominent tycoon has racked up tens of billions in disposals over the past few years, including the planned sale of his global ports, which would have netted about $19bn in cash but has run into a political storm because two of them are on the Panama Canal.

All of the wheeler-dealing raises questions about why the Li family wants to sell, what they plan to do with the money, and whether minority shareholders in their conglomerate, which trades at a sizeable discount to net asset value, will enjoy better returns.

Long-time watchers of CK Hutchison and its affiliated network of companies suspect this is not the prelude to a wider shake-up but rather the latest contrarian move by a savvy value investor, who will reinvest when he is ready.

“It’s not a bad moment to be long cash,” said one person familiar with the company in Hong Kong. “One thing for sure is they won’t hand it to the shareholders — it’s not the Asian way or the CKI way.”

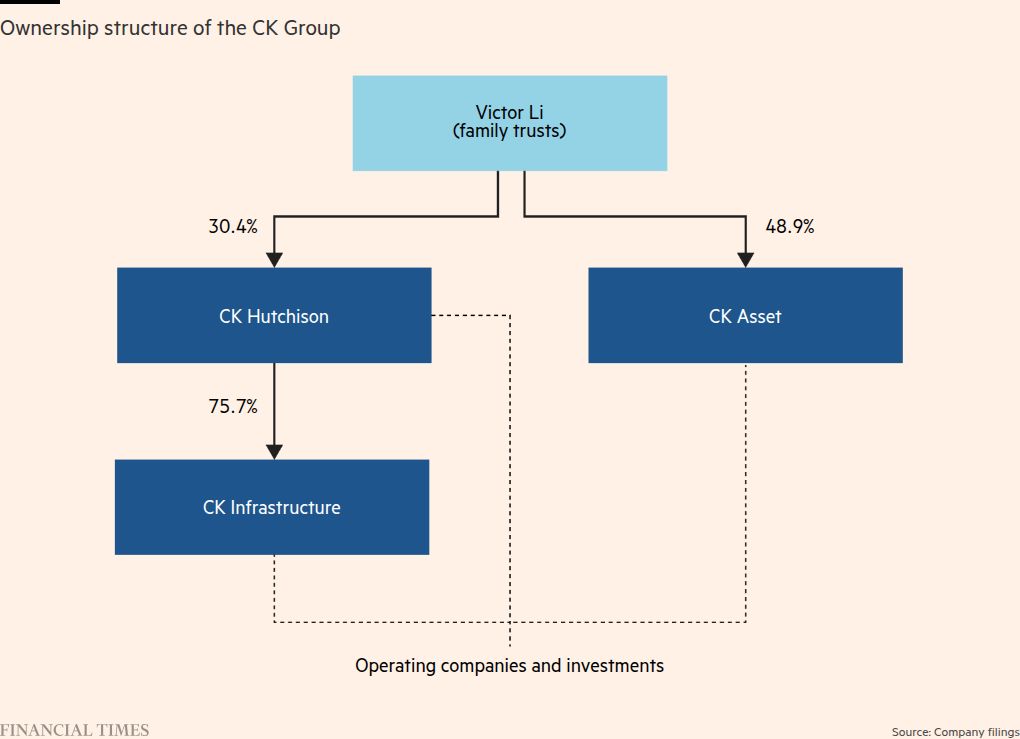

The family controls its empire through a complicated web of trusts and listed holding companies, of which CK Hutchison, CK Asset and CK Infrastructure are the most important. CK Hutchison did not respond to a request for comment.

Founded by combining the historic Hutchison Whampoa conglomerate with Li’s Cheung Kong property group, the company’s influence is epitomised by its stock code on the Hong Kong exchange: 0001.

Over the years, Li moved into retail, telecoms, energy and utilities, but recently he has turned seller.

The most recent deal was to exit UK Power Networks at an equity value of £10.5bn, more than three times the purchase price in 2010. It followed the £4bn sale of Eversholt Rail, one of the UK’s largest rolling stock lessors; the ports; and the merger of Three’s UK arm into Vodafone.

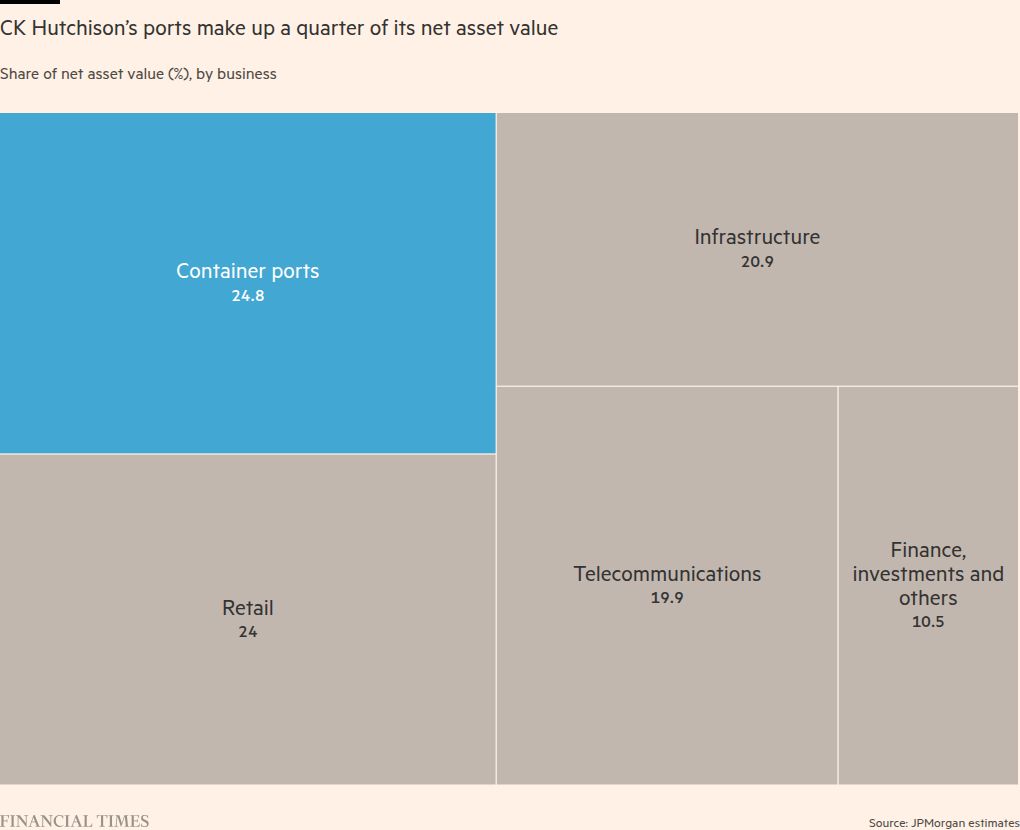

CK Hutchison is also mulling separate listings of its global telecommunications business and its retail division, which includes 830 Superdrug stores in the UK and Ireland. Both could have standalone valuations of as much as $30bn.

Now the question is what it does with its cash pile amid worsening geopolitical tensions and investor demands to return proceeds to shareholders.

According to analysts and advisers who work with the company, the disposals mirror CK’s style since Li Ka-shing first took control of Hutchison Whampoa in 1979.

“They go into brownfield [mature] assets that are badly run, improve them and eventually move on,” said one person familiar with their operations who did not have permission to speak publicly.

“They don’t buy to own forever. It’s rinse and repeat. These guys aren’t sentimental about stuff.”

In a clear sign of its ambition to resume dealmaking, the company said the UK Power Networks deal would generate “cash proceeds for future investments or acquisitions”. Management has told analysts it sees opportunities in European infrastructure.

Li, the conglomerate’s billionaire founder, was at one point Asia’s richest man. He passed day-to-day control of the company to his son Victor Li in 2018 — but the operating model is unchanged.

“People think they are a company. The reality is they are a conglomerate with very strong private equity characteristics, but the difference is PE has a shorter time horizon,” said a second person close to the company’s management.

Geopolitics has proven a barrier to entry for CK in recent years. In 2018, Israel turned down its bid to build a $1.5bn desalination plant, while CK Infrastructure in October labelled as “not market-led” the process by which struggling utility Thames Water chose KKR as its preferred bidder.

And in the most dramatic move yet, CK is now locked in arbitration with the Panamanian authorities after they voided its contracts to run the ports at either end of the Panama Canal.

Dan Baker, an analyst at Morningstar, said these incidents would make CK consider carefully whether future investments could incur the same issues.

“They don’t want that happening again — it would make sense that they’d be looking at assets in western markets that aren’t at risk of that,” he added.

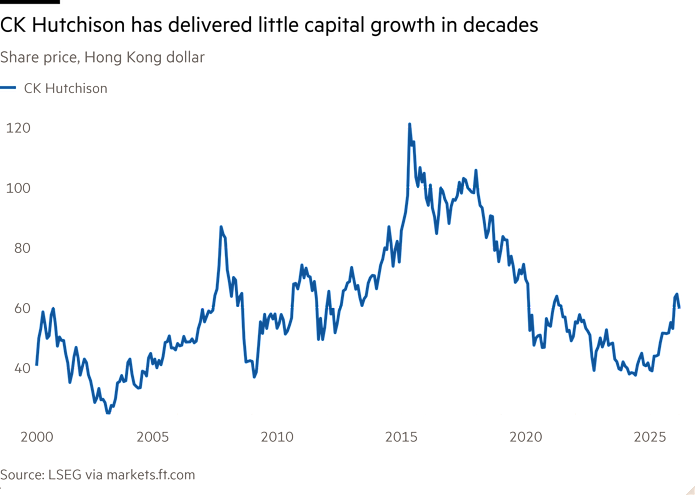

One bugbear for CK’s executives has been the share price, which trades at a substantial discount to the net asset value of its holdings.

At HK$59 per share, it trades at half the price it reached after a 2015 restructuring. The stated net asset value is HK$140.

“They’ve not been happy with the share price; there’s been a pretty heavy discount on where people would value the company,” said Baker.

This, he added, could be a rationale for listing more assets separately. “They’re going for more of a sum-of-the-parts type valuation.”

CK has not signalled that it intends to pay out the proceeds from recent sales as special dividends and share buybacks. Its implied dividend yield is close to 4 per cent — not far off HSBC, a favourite among Hong Kong’s income investors.

One shareholder said they thought that if CK was unable to locate fresh investment opportunities, they should look at buying back shares.

“If they don’t locate new investment opportunities, I’d be happy for them to distribute to shareholders or do share buybacks, given the discount to net asset value,” they said.

Other analysts are confident CK will hold on to its cash until it finds an opportunity worth springing for.

“If there’s an attractive acquisition opportunity, they’re willing to use the cash for M&A,” said Pierre Lau, an analyst at Citigroup.

“But this group, historically, is very patient; they don’t mind [missing] suitable opportunities, but they don’t want to overpay. They keep their eyes open.”

Data by Haohsiang Ko in Hong Kong